AIVaaS™ 7: Business Models Matter More to AI Than You Might Think

Adoption runs on operating models, transformation on business models.

In AIVaaS™, Designing New Business Models is not a creative exercise reserved for startups. It is the element that decides whether AI changes only how the business runs, or also the value it creates, and it begins far earlier than its place in the third pillar suggests.

The previous article ended with a business that was ready. Processes mapped to their decision points, data that caught the signal, a human at the decision that mattered. All of it prepared so that customers will be served well.

But does that last part hold? The processes and the data the previous article made ready belong to one place: the operating model, the way the business runs from day to day and what it offers as it runs.

Whether any of that movement also changed the value the business creates, and for whom, is a question readiness cannot answer.

The boardroom question is not only whether AI will make the business more efficient. It is whether AI will change what the business is worth, and to whom.

This article opens the second element of the third pillar, Designing New Business Models. The element sits late in the methodology. That placement hides how early its work begins.

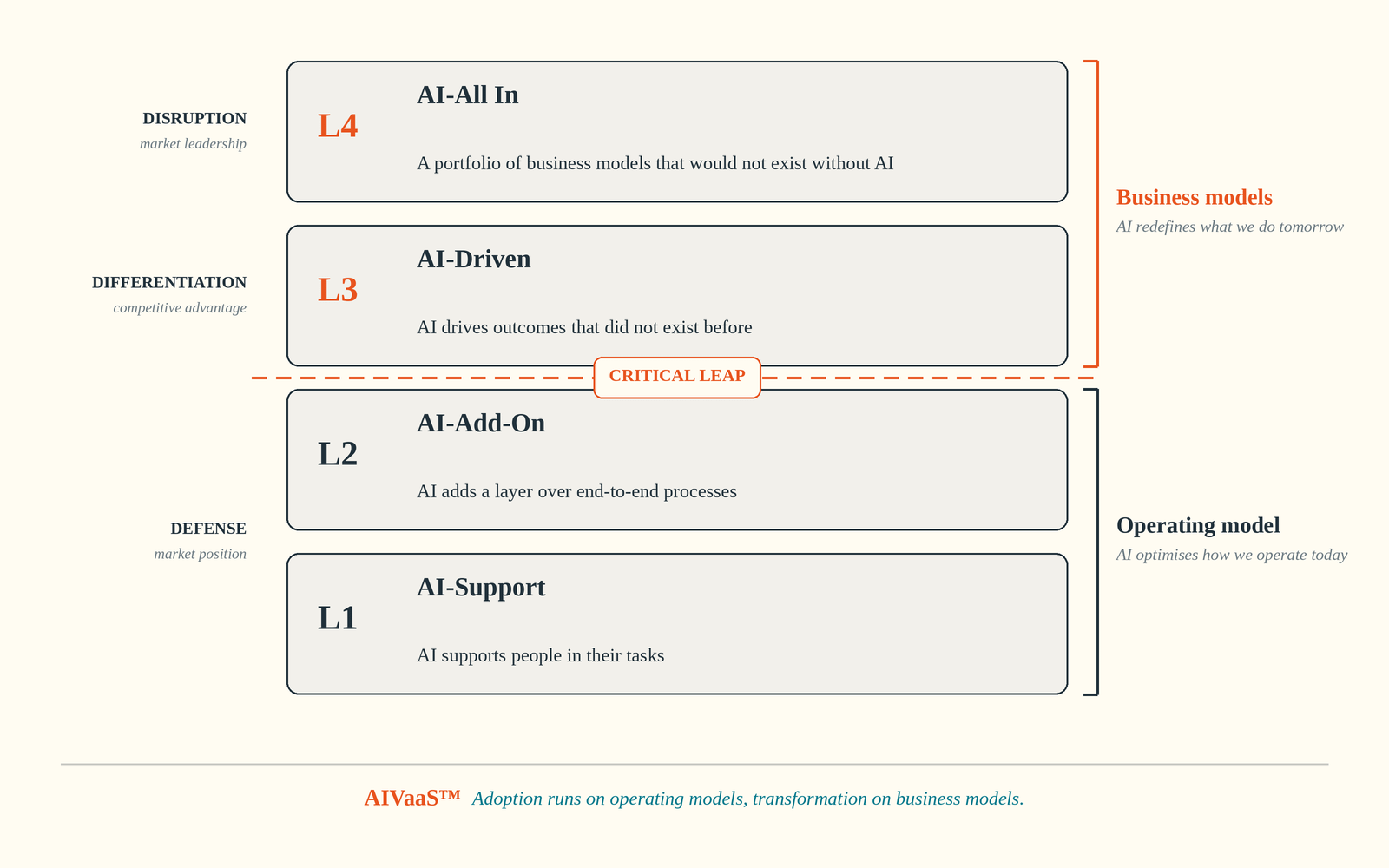

How early depends on AI ambition. Organisations aiming at L3 (AI-Driven) or L4 (AI-ALL IN), where AI drives outcomes the business could not produce before, meet business models at the strategy table, inside Ambition Fusion.

Organisations that entered at L1 (AI-Support) or L2 (AI Add-On) meet business models here, at the latest. For many boards this element is the final checkpoint where anyone asks whether the change in operations has quietly moved the business model too.

Even below the leap the question has weight. A manufacturer takes AI through sales and production and leaves logistics untouched. The gains are real, and unrealised: its customer measures value in deliveries that arrive in time for its own customers, at the address the programme never reached.

The organisations pulling ahead read this early. They run today’s operating model and build tomorrow’s business models beside it, in parallel, and the distance they gain compounds.

Business models were planted in this series long before this article, in its first economic reading, and every station since has returned to them.

Hidden in plain sight

The opening article placed Designing New Business Models on the map, as the second element of the third pillar, with one line attached: at higher ambition levels AI enables new ways of creating value.

The first economic reading went further. In the comparison of three economies, business models stand among the eight dimensions the shift moves: they change how value is captured.

The four levels of AI ambition lean on them harder. What separates L1 and L2 from L3 and L4 is whether business models move. At L4, the whole rests on a portfolio of business models that would not exist without AI.

The Value Creation Matrix runs on the same axis. Its lower row holds value created on the operating model, its upper row value created on the business model, and the critical leap runs between the rows.

Governance met the term from above. The deeper governance act is how far AI may go: support existing work, improve the operating model, reshape the value proposition, or enter the business strategy itself. Two rungs of that ladder live inside the business model.

And the previous article closed at its door: customer needs read from data, including needs no customer has voiced yet, are where new offers and new business models begin.

Six articles, and the term carried weight in every one, always in a supporting role. It stayed there because business models belong to the vocabulary every executive is assumed to know. That assumption deserves a test.

What a business model is

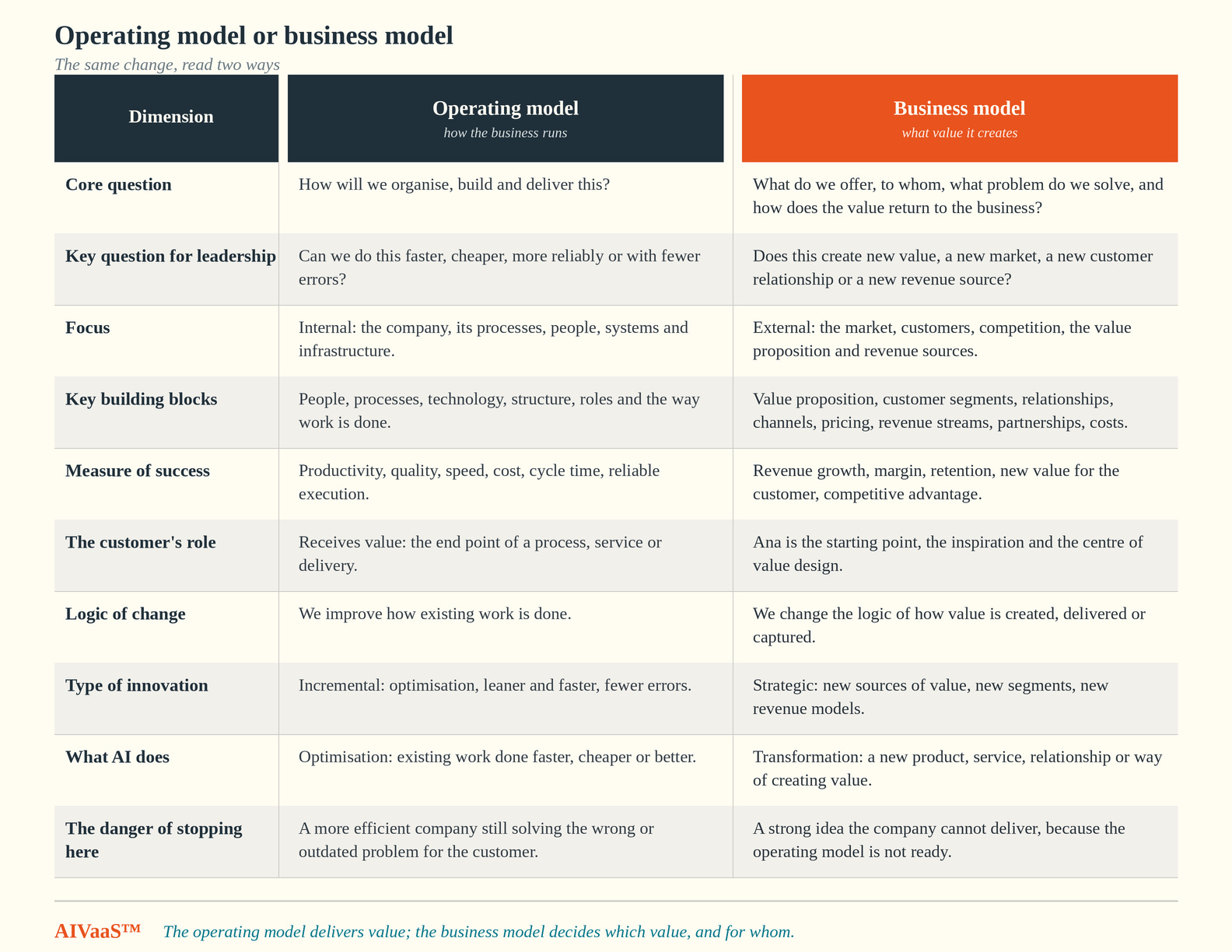

A business model is the rationale of how an organisation creates, delivers and captures value, for its customers and for itself. Three verbs, one noun, and the noun does the work.

Most management teams carry the term in the singular: the business model, one per company, decided long ago. The singular is the first thing to correct. Every organisation runs several business models at once, one for each customer segment and each distinct part of the offer.

The count settles a quieter fear. A new business model is added next to the existing ones, and the existing ones keep earning while it grows. Designing new business models threatens nothing that works today.

The definition and the working tool both come from Alexander Osterwalder. His Business Model Canvas describes each model in nine blocks and gives the several models of one organisation a shared page.

Five blocks face the market: customer segments, the value proposition at the centre, channels, customer relationships, revenue streams. Four face the engine room: key activities, key resources, key partnerships, cost structure.

The centre deserves its own instrument. The Value Proposition Canvas zooms into the fit between what the business offers and what the customer is trying to get done: the jobs, the pains, the gains. Where the two profiles meet, customer experience is won, and with it the value.

A second definition sharpens the horizon. Gennaro Cuofano reads a business model as a systematic way of unlocking long-term value while delivering it to customers and capturing part of it in return. The long term matters: models are designed to outlive the tools that enable them.

And the operating model? It has been on the canvas the whole time, in the engine room blocks: the key activities, key resources and key partnerships through which the value proposition gets delivered.

The two models divide the work.

The operating model holds how the business runs and delivers, its processes, people, systems and what it offers day to day. The business model reads the whole above it: which value, for whom, and how the value returns.

This is the test the opening question stands on. A change in operations enters the canvas through key activities and key resources. Whether it changed the business model depends on what moved above them: the proposition, the segments, the revenue logic.

Business models decide who disrupts

Osterwalder sorts innovation into three types. Efficiency innovation improves processes and the existing business model. Sustaining innovation extends value propositions into new channels and geographies. Transformative innovation builds new business models and new growth engines.

The sorting predicts the outcome. Disruptors work in the transformative class, where new models are born. The disrupted work in the efficiency class, polishing the model they already have, right up to the day it stops carrying them.

Behind the types sits an older pair. Exploit names the short horizon: efficiency, control, more profit from what exists. Explore names the long one: discovery, new revenue, new markets. L1 and L2 exploit, L3 and L4 explore, and the critical leap is the crossing between the two logics.

The pair is drawn with a plus sign, explore plus exploit, and the plus is the strategy: the strongest organisations refuse to choose between the two.

The third stage of digital business models

Digital business models divide into three stages. In the first, the organisation creates, delivers and captures value with the help of digital technologies: the model is enabled by digital, and the value itself can still be touched.

In the second stage the form of the value itself is digital. SaaS, Data as a Service, marketplace platforms, Direct-to-Fan models such as Substack: what the customer receives, uses and pays for exists as digital value, and the whole logic of the model follows it.

The third stage is opening now: digital business models based on AI. One of its clearest emerging forms is AGaaS, Agentic-as-a-Service.

Here digital value turns active. It delivers outcomes through work performed on its own, and the intelligence itself becomes the product: the next evolutionary stage of the digital business model.

For every company the question stands: which of its business models will AI enter, and which new ones will it make possible.

Where business models enter the AIVaaS™

Defined, the term returns to the methodology with weight. The first pillar touches business models before they become implementation work, and the third pillar inherits what the first has, or has not, prepared.

External Strategic AI Impact Analysis reads other people’s business models first: which competitors have moved to AI-native models, which adjacent industries can now enter, and where the value pool is migrating.

AI Ambition Alignment then chooses a response. Choosing L3 or L4 is choosing to design new business models; an ambition above the critical leap with no model design attached is a wish with a number on it.

AI Strategy Fusion keeps the design where it belongs. Business models are where strategy takes economic form: choices about value, customers, capabilities and revenue become a working model. AIVaaS™ knows no separate AI strategy; new models arise inside the AI-Infused Business Strategy.

Defining Stakeholder AI Opportunities gives each model its addresses, because opportunities in the two upper quadrants of the Value Creation Matrix are business model opportunities by definition. AI Investments Prioritization then distributes the portfolio between exploit and explore. An empty Q4 in an environment that demands transformation now has a second name: no new business model in design.

The Foundation validates the model before deployment. Value & ROI Validation runs from the first pillar on: created, delivered and captured value are named and tested while the model is still a design.

AI Governance gains a portfolio to govern: which models are added, which coexist, and which are retired. Adding a model changes what the business is, and that decision belongs to leadership. Continuous Capability Growth closes the loop, because business model innovation with AI is now a permanent capability, not a one-off exercise.

The leap runs through the business model

The critical leap between L2 and L3 has appeared in this series as a leap of ambition, of posture, of governance and of readiness. This article adds the shortest description it has: the leap is where the business model starts to move.

What moves with it is the competitive position. Below the leap the organisation plays defence: gains on the operating model protect the market position it already holds, and every competitor is running the same programmes.

Above the leap the position itself starts to move: towards differentiation and competitive advantage at L3, towards disruption and market leadership at L4. The reward of real AI transformation lives there, the breakthrough to the leading position in the market and with the customer.

The levels are levels of ambition, and no rule says they must be climbed in order. Because a new business model rises beside the running operation rather than through it, an organisation can hold its position at L1 and L2 while building at L3 or L4 in parallel.

For organisations aiming at L3 or L4, the design work belongs to the first pillar, inside the strategy and the validation that runs with it. For organisations at L1 and L2, this element is the last checkpoint: the place to ask, once, what the readiness work has moved.

The answer can be nothing, and nothing is a legitimate answer. The check exists because the other answer arrives uninvited: processes and data redesigned around new decisions can shift a value proposition without anyone deciding they should.

Either way, the question has left the technical floor. What the business is worth, and to whom, is being decided again. And the first to register the outcome is not anyone inside the organisation.

Ana feels it first

In the stories that opened this series, Ana is the customer the organisation serves today, and the child she is carrying is the customer of the next, more intelligent economy.

Ana does not wake up with a wish to buy something. She wakes up into a life that changed three days ago, with needs she is only beginning to sense. Value, for her, starts in the need.

Everything this article has described, the canvas, the stages, the portfolio, is invisible to Ana. What reaches her is the answer itself: whether a need of hers is met, how completely, and at what cost in money, time and trust.

The product she meets comes from the operating model; the value she experiences, from the business model. When only the operating model improves, a need she already had is answered a little better.

A new business model reaches further. It answers a need that had no answer, sometimes a need she has not yet voiced, and she registers that before any internal metric does.

That is what her sentence on the phone meant. Buying completely different things describes a life reorganising itself into new needs, before any product has a name. The businesses designing new models around those needs are the ones that will exist in her new life.

Ana does not experience an operating model. She experiences whether the business model has made room for her new life. That is why the critical leap runs through the business model, not around it.